Research - (2021) Volume 10, Issue 6

Received: 03-Jun-2021

Published:

29-Jun-2021

, DOI: 10.37421/2168-9601.2021.10.331

Citation: Selvaraj N. "Customer Service in Banks and Its Importance in Tamilnadu." J Account Mark 10 (2021): 331.

Copyright: © 2021 Selvaraj N. This is an open-access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

The problems in promoting of bank services in urban and semi-urban square measureas are completely different. The sort of services needed differs in urban and rural square measureas and stratified services are required within the industry. Folks have a large selection of services and a multiplicity of product desires. However they're continually tuned in to convenience, cost, safety, speed, respect, quality, courtesy and class. The current day bankers got to reply to the wants of the shoppers during this intensely competitive and quickly ever-changing atmosphere. A bank is an establishment that deals with cash and credit. For a standard man, a bank suggests that a store house of cash, for a bourgeois it's an establishment of finance and for every day to day client it's a facility for his savings. Truly banks square measure business organizations commercialism bank services. Banks play a significant role to serve the folks and improve the economy of any country. Now-days, banking sector acts because the backbone of recent business. Development of any country chiefly depends upon the banking industry. A bank could be a financial organization that deals with deposits and advances and different connected services. The promotional measures like personal commercialism, loan melas, ad through newspapers, co-operative bank workers, the posters and pamphlets could also be increased so as to retain existing customers and attract new customers within the state. Regular feedbacks ought to be taken by the shoppers regarding the operating of the banks such feedback offers Associate in nursing insight of shopper’s expectation from banks and offers scope for any improvement. Within the days to come back, banks square measure expected to play a really vital role within the economic development and therefore the rising market can give business and promoting opportunities to harness. As banking in Asian nation can become additional and additional information supported, capital can emerge because the finest assets of the banking industry.

Banks • Customers • Development • Fashionable business and client perspective

The problems in promoting of bank services in urban and semi-urban square measure as are completely different. The sort of services needed differs in urban and rural square measure as and stratified services are required within the industry. Folks have a large selection of services and a multiplicity of product desires. However they're continually tuned in to convenience, cost, safety, speed, respect, quality, courtesy and class. The current day bankers got to reply to the wants of the shoppers during this intensely competitive and quickly ever-changing atmosphere. Any extra amendment or maybe amendment within the work state of affairs could also be opposed by the personnel, however to form the shoppers feel that they're distinctive, the personnel square measure to be trained properly so they'll give fairly cautious, friendly and intimate services to the shoppers. It’s not continually simple to live satisfaction of the shoppers because the term itself is very subjective. Varied services square measure to be known and measured within the order of importance and therefore the accessibility of such services to the shoppers is to be measured. Within the light-weight of the issues listed higher than, the current study tries a promoting of banking services in Taminadu.

Statement of the Problem

A bank is an establishment that deals with cash and credit. For a standard man, a bank suggests that a store house of cash, for a bourgeois it's an establishment of finance and for every day to day client it's a facility for his savings. Truly banks square measure business organizations commercialism bank services. Banks play a significant role to serve the folks and improve the economy of any country. Banks hold the savings of the general public give a way of payment permanently and services and finance development of the business and trade. So banks act as Associate in nursing negotiate within the flow of funds from server to users. Therefore, banks ought to render Associate in nursing economical client service, to retain the current customers and conjointly to draw in potential customers. It’s imperative to integrate the promoting of banking services and customers’ expectations however conjointly evaluating ways that and suggests that to improvise the banking services supported the customers’ perceptions on the perspective towards the service system of the banks. This study analyses such a tangle. Therefore the study was undertaken to know the assorted factors in terms of promoting of banking services in Tamilnadu.

Objectives of the Study

The confined objectives of the current study are: 1. To reveal a summary of the promoting of banking services. 2. To supply suggestions for improvement of banking services on the idea of findings of the study.

Period of the Study

The period of the study ranges from Gregorian calendar month 2018 to Gregorian calendar month 2019.

Research methodology could be scientific and systematic thanks to solve analysis issues. The analysis methodology deals with analysis strategies and brought into thought the logic behind the strategies. In total, the analysis methodology of the study includes analysis style, sampling framework, knowledge assortment, framework of research and limitations. Sources of information the current study is totally supported the first knowledge. The secondary knowledge collected from the books, journals, magazines and websites were wont to kind the theoretical framework of the study and therefore the review of literature. The first knowledge was collected in person with the assistance of structured form.

Shanker Shetty [1] has unconcealed in his study that the longer term promoting strategy for banks ought to imbibe making Associate in Nursing economical value effective, courteous, product together with an efficient delivery system, that ought to pay attention of the buyer’s selections because the deciding issue of the fortunes of banks within the future. Gopalakrishnan [2] within the fashionable competitive world, banks got to resolve the wants of the shoppers and create them obtainable at competitive value at once. The wants of various segments square measure to be addressed singly and applicable schemes square measure to be introduced to stay within the market [3]. It’s for the banks to alter the attitude of shoppers and infuse confidence in them that the banks square measure reliable future partners. Interaction with the shoppers at regular intervals to search out their necessities and create them obtainable would go a protracted manner in creating the organizations to survive during this ferociously competitive world. Phone calls square measure needed to be attended promptly and queries processed on the spot as way as doable [4].

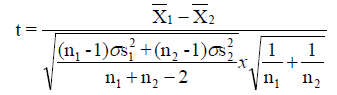

T-Test

The‘t’ test is used to find out the significant difference among the two group of samples regarding any intention variable which is internal scale. The‘t’ statistics is calculated by

Degree of freedom of (n1 + n2 – 2)

Whereas t – ‘t’ statistics

X1 – Mean of the first sample

X2 – Mean of the second sample

σ12 – Variance in the first sample

σ22 – Variance in the second sample

n1 – Number of samples in first group

n2 – Number of samples in second group

In the study, the‘t’ test has been used to find out the significant difference between gender and family type with respect to deficiencies in banking services and improvement in banking services.

Opinion of the Respondents

Ranking for client Awareness on Bank Schemes issue In this study, client Awareness on Bank Schemes accommodates 10 factors that live oldster Deposit Schemes, company Liquid Term Deposit, accounting Deposit, Tax saving deposit, Deposit Schemes for NRI’S (NRE & NRO), mounted Deposit, Savings checking account, Capital Gains and Term Deposit. The table below shows the ranking for things |the things} comprising the client Awareness on Bank Schemes that constitutes ten items. Things were skilled on a five purpose Likert scale starting from ‘Fully Aware’ to ‘Not Aware at all’. Ranking has been done supported the mean values.

Table 1 shows that “Senior national Deposit Schemes” is that the top hierarchic client Awareness on Bank Schemes issue with a norm of 4.11, “Corporate Liquid Term Deposit” is that the second hierarchic client Awareness on Bank Schemes issue with a norm of 4.10, “Current Account Deposit” is that the third hierarchic client Awareness on Bank Schemes issue with a norm of 4.09, “Tax saving deposit” is that the fourth hierarchic client Awareness on Bank Schemes issue with a norm of 4.07, “Recurring Deposit” is that the fifth hierarchic client Awareness on Bank Schemes issue with a norm of 4.06, “Deposit Schemes for NRI’S (NRE & NRO)” is that the sixth hierarchic client Awareness on Bank Schemes issue with a norm of 3.75, “Fixed Deposit” is that the seventh hierarchic client Awareness on Bank Schemes issue with a norm of 3.69, “Savings Bank Account” is that the eighth hierarchic client Awareness on Bank Schemes issue with a norm of 3.67, “Capital Gains Plus” is that the ninth hierarchic client Awareness on Bank Schemes issue with a norm of 3.66 and “Term Deposit” is that the tenth hierarchic client Awareness on Bank Schemes issue with a norm of 3.64. Ranking for General Utility (or) Miscellaneous Service issue In this study, General Utility (or) Miscellaneous Service accommodates 9 factors that live Credit Cards / Debit Cards, payment of Fund, assortment of Cheque / Draft, Gift Cheque, Safety Locker, Loan facility, businessperson Banking, Government Schemes and Cheque drop box. The table below shows the ranking for things|the things} comprising the final Utility (or) Miscellaneous Service that constitutes nine items. Things were skilled on a five purpose Likert scale starting from ‘Fully Aware’ to ‘Not Aware at all’. Ranking has been done supported the mean values.

| Customer Awareness on Bank Schemes | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| Senior Citizen Deposit Schemes | 4.11 | .646 | -.108 | -.627 |

| Corporate Liquid Term Deposit | 4.10 | .653 | -.229 | -.217 |

| Current Account Deposit | 4.09 | .636 | -.077 | -.545 |

| Tax saving deposit | 4.07 | .686 | -.412 | .189 |

| Recurring Deposit | 4.06 | .626 | -.045 | -.453 |

| Deposit Schemes for NRI’S (NRE & NRO) | 3.75 | .681 | -.031 | -.267 |

| Fixed Deposit | 3.69 | .673 | -.085 | -.160 |

| Savings Bank Account | 3.67 | .631 | .267 | -.533 |

| Capital Gains Plus | 3.66 | .637 | .181 | -.421 |

| Term Deposit | 3.64 | .611 | -.061 | -.242 |

Table 2 shows that “Credit Cards / Debit Cards” is that the top hierarchic General Utility (or) Miscellaneous Service issue with a norm of 4.21, “Remittance of Fund” is that the second hierarchic General Utility (or) Miscellaneous Service issue with a norm of 4.15, “Collection of Cheque / Draft” is that the third hierarchic General Utility (or) Miscellaneous Service issue with a norm of 4.11, “Gift Cheque” is that the fourth hierarchic General Utility (or) Miscellaneous Service issue with a norm of 4.02, “Safety Locker” is that the fifth hierarchic client General Utility (or) Miscellaneous Service issue with a norm of 3.63, “Loan facility” is that the sixth hierarchic General Utility (or) Miscellaneous Service issue with a norm of 3.58, “Merchant Banking” is that the seventh hierarchic General Utility (or) Miscellaneous Service issue with a norm of 3.55, “Government Schemes” is that the eighth hierarchic General Utility (or) Miscellaneous Service issue with a norm of 3.48, and “Cheque drop box” is that the ninth hierarchic General Utility (or) Miscellaneous Service issue with a norm of 3.24. Ranking for Agency Service issue In this study, Agency Service accommodates 10 factors that live soul Card, Payment of EB Bill, Payment of MasterCard, Payment of LIC Premium, Payment of tax, Payment of Corporation Tax, Payment of Insurance Premium, Payment of Subscription, Rent, Rates, and Taxes, Others (Please specify) and assortment of money / Cheque / Draft. The table below shows the ranking for things|the things} comprising the Agency Service that constitutes ten items. Things were skilled on a five purpose Likert scale starting from ‘Fully Aware’ to ‘Not Aware at all’. Ranking has been done supported the mean values.

| General Utility (or) Miscellaneous Service | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| Credit Cards / Debit Cards | 4.21 | .631 | -.195 | -.609 |

| Remittance of Fund | 4.15 | .693 | -.209 | -.917 |

| Collection of Cheque / Draft | 4.11 | .750 | -.582 | .112 |

| Gift Cheque | 4.02 | .785 | -.806 | 1.398 |

| Safety Locker | 3.63 | .570 | .229 | -.758 |

| Loan facility | 3.58 | .738 | -.076 | -.279 |

| Merchant Banking | 3.55 | .770 | .238 | -.440 |

| Government Schemes | 3.48 | .764 | .057 | -.354 |

| Cheque drop box | 3.24 | 1.001 | -.307 | -.123 |

Table 3 shows that “Traveller Card” is that the top hierarchic Agency Service issue with a norm of 4.10, “Payment of EB Bill” is that the second hierarchic Agency Service issue with a norm of 3.81, “Payment of Credit card” is that the third hierarchic Agency Service issue with a norm of 3.80, “Payment of LIC Premium” is that the fourth hierarchic Agency Service issue with a norm of 3.76, “Payment of financial gain Tax” is that the fifth hierarchic Agency Service issue with a norm of 3.74, “Payment of Corporation Tax” is that the sixth hierarchic Agency Service issue with a norm of 3.68, “Payment of Insurance Premium” is that the seventh hierarchic Agency Service issue with a norm of 3.62, “Payment of Subscription, Rent, Rates, and Taxes” is that the eighth hierarchic Agency Service issue with a norm of 3.60, “Others (Please specify)” is that the ninth hierarchic Agency Service issue with a norm of three.60 and “Collection of money / Cheque / Draft” is that the tenth hierarchic Agency Service issue with a norm of 3.47. Ranking for Innovative Service issue in this study, Agency Service encompass 10 factors that live E-Lobby, web Banking, Mobile Banking, E – Pay, Pass Book, Gift card, on-line Service, MasterCard, Tele – Banking and Fuel card (Prepaid card). The table below shows the ranking for things the things} comprising the Innovative Service issue that constitutes ten items. things were tried and true on a five purpose Likert scale starting from ‘Fully Aware’ to ‘Not Aware at all’. Ranking has been done supported the mean values.

| Agency Service | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| Traveler Card | 4.10 | .700 | -.243 | -.613 |

| Payment of EB Bill | 3.81 | .776 | -.393 | .297 |

| Payment of Credit card | 3.80 | .728 | .233 | -.920 |

| Payment of LIC Premium | 3.76 | .583 | .092 | -.442 |

| Payment of Income Tax | 3.74 | .768 | -.196 | .087 |

| Payment of Corporation Tax | 3.68 | .701 | .434 | -.751 |

| Payment of Insurance Premium | 3.62 | .696 | .378 | -.509 |

| Payment of Subscription, Rent, Rates, and Taxes | 3.60 | .730 | .255 | -.448 |

| Others (Please specify) | 3.60 | .595 | .432 | -.675 |

| Collection of Cash / Cheque / Draft | 3.47 | .759 | .212 | .095 |

Table 4 shows that “E-Lobby” is that the top hierarchic Innovative Service issue with a norm of 4.74, “Net Banking” is that the second hierarchic Innovative Service issue with a norm of 4.21, “Mobile Banking” is that the third hierarchic Innovative Service issue with a norm of four.05, “E – Pay ” is that the fourth hierarchic Innovative Service issue with a norm of 4.03, “Pass Book” is that the fifth hierarchic Innovative Service issue with a norm of 3.92, “Gift card” is that the sixth hierarchic Innovative Service issue with a norm of 3.74, “Online Service” is that the seventh hierarchic Innovative Service issue with a norm of 3.73, “Credit Card” is that the eighth hierarchic Innovative Service issue with a norm of 3.69, “Tele Banking” is that the ninth hierarchic Innovative Service issue with a norm of 3.48 and “Fuel card (Prepaid card)” is that the tenth hierarchic Innovative Service issue with a norm of 3.37. Ranking for client perspective towards Services of Banks issue In this study, client perspective towards Services of Banks encompass 10 factors that live New Service Offered by Banks area unit well-known Through Bank workers at the Branch, there's Accessibility to the Bank, the purchasers Meet Improves the standard of Service Rendered by the Bank, Charges Levied by Banks for various Service or affordable, whether or not operating day is appropriate, client central, Business Hours is appropriate, Rate of Interest on Loan is cheap, The Work of the one Window System Expedites dealing and Time Taken for bank services. The table below shows the ranking for things thecomprising the client perspective towards Services of Banks issue that constitutes ten items. Things were tried and true on a five purpose Likert scale starting from ‘Strongly Agree’ to ‘Strongly Disagree’. Ranking has been done supported the mean values.

| Innovative Service | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| E-Lobby | 4.74 | .564 | -2.748 | 9.240 |

| Net Banking | 4.21 | .703 | -.325 | -.954 |

| Mobile Banking | 4.05 | .972 | -.515 | -1.004 |

| E – Pay | 4.03 | .951 | -.197 | -1.573 |

| Pass Book | 3.92 | 1.039 | -.486 | -.572 |

| Gift card | 3.74 | .935 | -.348 | -.726 |

| Online Service | 3.73 | 1.201 | -.662 | -.487 |

| Credit Card | 3.69 | 1.124 | -.678 | -.084 |

| Tele – Banking | 3.48 | .970 | -.294 | .135 |

| Fuel card (Prepaid card) | 3.37 | .744 | .100 | -.285 |

Table 5 shows that “New Service Offered by Banks area unit well-known Through Bank workers at the Branch” is that the top hierarchic client perspective towards Services of Banks issue with a norm of 3.95, “There is Accessibility to the Bank” is that the second hierarchic client perspective towards Services of Banks issue with a norm of 3.80, “The clients Meet Improves the standard of Service Rendered by the Bank” is that the third hierarchic Customer perspective towards Services of Banks issue with a norm of 3.66, “Charges Levied by Banks for various Service or Reasonable” is that the fourth hierarchic client perspective towards Services of Banks issue with a norm of 3.61, “Whether operating day is suitable” is that the fifth hierarchic client perspective towards Services of Banks issue with a norm of 3.56, “Customer centric” is that the sixth hierarchic client perspective towards Services of Banks issue with a norm of three.46, “Business Hours is Suitable” is that the seventh hierarchic client perspective towards Services of Banks issue with a norm of 3.40, “Rate of Interest on Loan is Reasonable” is that the eighth hierarchic client perspective towards Services of Banks issue with a norm of 3.28, “The Work of the one Window System Expedites Transaction” is that the ninth hierarchic client perspective towards Services of Banks issue with a norm of 3.25 and “Time Taken for bank services” is that the tenth hierarchic client perspective towards Services of Banks issue with a norm of 3.11. Ranking for Responsiveness issue In this study, Responsiveness encompass 9 factors that live issue in Mobile Banking Services, an excessive amount of of Collateral Securities, Difficulties in victimization e-lobbies, Delayed Payments, Lack of awareness, Poor Response to Grievances, Behavior of employees in counter, Rigid Rules and rules and Time taken for rendering services. The table below shows the ranking for things thecomprising the Responsiveness issue that constitutes nine items. Things were tried and true on a five purpose Likert scale starting from ‘Highly Satisfied’ to ‘Highly Dissatisfied’. Ranking has been done supported the mean values.

| Customer Attitude towards Services of Banks | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| New Service Offered by Banks are Known Through Bank Employees at the Branch | 3.95 | 1.269 | -1.068 | .013 |

| There is Accessibility to the Bank | 3.80 | .984 | -.492 | -.201 |

| The Customers Meet Improves The Quality of Service Rendered by the Bank | 3.66 | 1.050 | -.416 | -.653 |

| Charges Levied by Banks for Different Service or Reasonable | 3.61 | 1.184 | -.467 | -.852 |

| Whether working day is suitable | 3.56 | .828 | -.739 | .725 |

| Customer centric | 3.46 | 1.098 | -.342 | -.716 |

| Business Hours is Suitable | 3.40 | 1.005 | -.866 | .481 |

| Rate of Interest on Loan is Reasonable | 3.28 | 1.281 | -.367 | -.814 |

| The Work of the Single Window System Expedites Transaction | 3.25 | .908 | -.206 | .149 |

| Time Taken for bank services | 3.11 | 1.340 | -.207 | -1.057 |

Table 6 shows that “Difficulty in Mobile Banking Services” is that the top hierarchic Responsiveness issue with a norm of 4.29, “Too a lot of Collateral Securities” is that the second hierarchic Responsiveness issue with a norm of 3.83, “Difficulties in victimization e-lobbies” is that the third hierarchic Responsiveness issue with a norm of 3.74, “Delayed Payments” is that the fourth hierarchic Responsiveness issue with a norm of 3.51, “Lack of awareness” is that the fifth hierarchic Responsiveness issue with a norm of 3.39, “Poor Response to Grievances” is that the sixth hierarchic Responsiveness issue with a norm of 3.38, “Behavior of employees in counter” is that the seventh hierarchic Responsiveness issue with a norm of 3.37, “Rigid Rules and Regulations” is that the eighth hierarchic Responsiveness issue with a norm of 3.30 and “Time taken for rendering services” is that the ninth hierarchic Responsiveness issue with a norm of 3.12. Ranking for Assurance issue In this study, Assurance consists of two factors that live Lack of employees Strength and Poor in Personal Attention. The table below shows the ranking for things |the things} comprising the reassurance that constitutes a pair of items. Things were tried and true on a five purpose Likert scale starting from ‘Highly Satisfied’ to ‘Highly Dissatisfied’. Ranking has been done supported the mean values.

| Responsiveness | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| Difficulty in Mobile Banking Services | 4.29 | .759 | -.548 | -1.073 |

| Too Much of Collateral Securities | 3.83 | .837 | -1.366 | 3.233 |

| Difficulties in using e-lobbies | 3.74 | 1.016 | -.025 | -1.276 |

| Delayed Payments | 3.51 | 1.026 | -.391 | -.208 |

| Lack of awareness | 3.39 | 1.037 | -.220 | -.426 |

| Poor Response to Grievances | 3.38 | 1.131 | -.277 | -.361 |

| Behaviour of staff in counter | 3.37 | 1.112 | -.257 | -.562 |

| Rigid Rules and Regulations | 3.30 | 1.198 | -.102 | -.809 |

| Time taken for rendering services | 3.12 | 1.285 | -.225 | -.915 |

Table 7 shows that “Lack of employees Strength” is that the top hierarchic Assurance issue with a norm of 4.03, “Poor in Personal Attention” is that the second hierarchic Assurance issue with a norm of three.57 Ranking for Charges issue In this study, Charges encompass four factors that live No monetary practice Services offered, Frequent High Service Charges, No would like primarily based Finance / education loan and Favoritism. The table below shows the ranking for things|the things} comprising the fees that constitutes four items. Things were tried and true on a five purpose Likert scale starting from ‘Highly Satisfied’ to ‘Highly Dissatisfied’. Ranking has been done supported the mean values.

| Assurance | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| Lack of Staff Strength | 4.03 | 1.082 | -.927 | -.069 |

| Poor in Personal Attention | 3.57 | 1.222 | -.474 | -.603 |

Table 8 shows that “No monetary practice Services available” is that the top hierarchic Charges issue with a norm of 3.75, “Frequent High Service Charges” is that the second hierarchic Charges issue with a norm of 3.48, “No would like primarily based Finance / education loan” is that the third hierarchic Charges issue with a norm of 3.47 and “Favouritism” is that the fourth hierarchic Charges issue with a norm of three.26. Ranking for Facilities issue in this study, Facilities encompass 2 factors that live inadequate no. of ATM Facilities and Inadequate car parking zone. The table below shows the ranking for things |the things} comprising the Facilities that constitutes a pair of items. Things were tried and true on a five purpose Likert scale starting from ‘Highly Satisfied’ to ‘Highly Dissatisfied’. Ranking has been done supported the mean values.

| Charges | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| No Financial Consultancy Services available | 3.75 | 1.108 | -.214 | -1.346 |

| Frequent High Service Charges | 3.48 | 1.083 | -.271 | -.605 |

| No Need Based Finance / education loan | 3.47 | 1.064 | -.339 | -.491 |

| Favouritism | 3.26 | 1.205 | -.394 | -.619 |

Table 9 shows that “Inadequate no. of ATM Facilities” is that the prime hierarchic Facilities issue with a norm of 4.36, “Inadequate Parking space” is that the second hierarchic Facilities issue with a norm of 2.64. Ranking for house issue In this study, house consists of 2 factors that live No adequate Place for Sitting and Distance between home and bank. The table below shows the ranking for things|the things} comprising the house that constitutes a pair of items. things were tried and true on a five purpose Likert scale starting from ‘Highly Satisfied’ to ‘Highly Dissatisfied’. Ranking has been done supported the mean values.

| Facilities | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| Inadequate no. of ATM Facilities | 4.36 | .590 | -.310 | -.685 |

| Inadequate Parking space | 2.64 | 1.297 | .089 | -1.276 |

Table 10 shows that “No adequate Place for Sitting” is that the top hierarchic house issue with a norm of 3.64 and “Distance between home and bank” is that the second hierarchic house issue with a norm of 3.60. Ranking for Strategy issue in this study, Strategy encompass 2 factors that live Educate / Conduct awareness camps / program for the purchasers and Accuracy of data provided by the bank. The table below shows the ranking for things|the things} comprising the Strategy that constitutes a pair of items. Things were tried and true on a five purpose Likert scale starting from ‘Highly Satisfied’ to ‘Highly Dissatisfied’. Ranking has been done supported the mean values.

| Space | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| No adequate Place for Sitting | 3.64 | 1.234 | -.839 | -.216 |

| Distance between home and bank | 3.60 | .893 | -.131 | -.718 |

Table 11 shows that “Educate / Conduct awareness camps / program for the customers” is that the top hierarchic Strategy issue with a norm of 4.12 and “Accuracy of data provided by the bank” is that the second hierarchic Strategy issue with a norm of 3.29. Ranking for Facilities issue in this study, Facilities encompass 5 factors that live board / tally pointers, Locker facilities / sitting facilities, Improve the operating atmosphere to form customers feel snug, simple microscope and Ramp facilities for disable individuals. The table below shows the ranking for things|the things} comprising the Facilities that constitutes five items. things were tried and true on a five purpose Likert scale starting from ‘Highly Satisfied’ to ‘Highly Dissatisfied’. Ranking has been done supported the mean values.

| Strategy | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| Educate / Conduct awareness camps / program for the customers | 4.12 | .818 | -.444 | -.786 |

| Accuracy of information provided by the bank | 3.29 | 1.179 | -.237 | -.543 |

Table 12 shows that “Notice Board / tally Guidelines” is that the top hierarchic Facilities issue with a norm of 3.60, “Locker facilities / sitting facilities” is that the second hierarchic Facilities issue with a norm of 3.54, “Improve the operating atmosphere to form customers feel comfortable” is that the third hierarchic Facilities issue with a norm of 3.41 “Magnifying glass” is that the fourth hierarchic Facilities issue with a norm of 3.28 and “Ramp facilities for disable people” is that the fifth hierarchic Facilities issue with a norm of 2.91. Ranking for Orientation issue In this study, Orientation encompass 2 factors that live coaching programmes to be organized for the purchasers – relating to use of Mobile Banking/E-Banking System / ATM and Special attention to encourage / encourage the purchasers to repay the loan. The table below shows the ranking for things|the things} comprising the Orientation that constitutes a pair of items. things were tried and true on a five purpose Likert scale starting from ‘Highly Satisfied’ to ‘Highly Dissatisfied’. Ranking has been done supported the mean values.

| Facilities | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| Notice Board / RBI Guidelines | 3.60 | 1.042 | -.321 | -.660 |

| Locker facilities / sitting facilities | 3.54 | .858 | .062 | -.651 |

| Improve the working environment to make customers feel comfortable | 3.41 | 1.078 | .076 | -.893 |

| Magnifying glass | 3.28 | 1.161 | .044 | -1.052 |

| Ramp facilities for disable people | 2.91 | 1.166 | .165 | -.923 |

Table 13 shows that “Training programmes to be organized for the shoppers – relating to use of Mobile Banking/E-Banking System / ATM” is that the top stratified Orientation issue with a average of 3.76 and “Special attention to inspire / encourage the shoppers to repay the loan” is that the second stratified Orientation issue with a average of 3.12. Ranking for data issue In this study, data incorporates 2 factors that live Separate counter for every activities (Deposits, withdrawals and Loans) and while not data of client permission. The table below shows the ranking for things|the things} comprising the Orientation that constitutes two items. things were older on a five purpose Likert scale starting from ‘Highly Satisfied’ to ‘Highly Dissatisfied’. Ranking has been done supported the mean values.

| Orientation | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| Training programmes to be arranged for the customers – regarding use of Mobile Banking/E-Banking System / ATM | 3.76 | 1.111 | -1.292 | 1.263 |

| Special attention to motivate / encourage the customers to repay the loan | 3.12 | 1.125 | -.320 | -.778 |

Table 14 shows that “Separate counter for every activities (Deposits, withdrawals and Loans)” is that the high stratified data issue with an average of 3.75 and “Without data of client permission” is that the second stratified data issue with an average of 3.23. Ranking for fellow feeling issue. In this study, fellow feeling incorporates 2 factors that live A separate cell for redressel of grievances and Improve the publication and advertisements concerning the bank and its product and services area unit high enough to adequately unfold shopper awareness. The table below shows the ranking for things |the things} comprising the fellow feeling that constitutes two items. Things were older on a five purpose Likert scale starting from ‘Highly Satisfied’ to ‘Highly Dissatisfied’. Ranking has been done supported the mean values.

| Knowledge | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| Separate counter for each activities (Deposits, withdrawals and Loans) | 3.75 | .968 | -.417 | -.764 |

| Without knowledge of customer permission | 3.23 | .881 | .379 | .318 |

Table 15 shows that “Se A separate cell for redressel of grievances” is that the top stratified fellow feeling issue with an average of 4.25 and “Improve the publication and advertisements concerning the bank and its product and services area unit high enough to adequately unfold shopper awareness” is that the second stratified fellow feeling issue with a average of 3.60. Ranking for Responsiveness issue in this study, Responsiveness incorporates 3 factors that live Special banking is given to enhance the performance of the bank workers, scale back the waiting time and Offers a range of engaging loans and deposit schemes. The table below shows the ranking for things |the things} comprising the Responsiveness that constitutes three items. Things were older on a five purpose Likert scale starting from ‘Highly Satisfied’ to ‘Highly Dissatisfied’. Ranking has been done supported the mean values.

| Empathy | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| A separate cell for redressel of grievances | 4.25 | .734 | -.706 | .119 |

| Improve the publication and advertisements about the bank and its products and services are high enough to adequately spread consumer awareness | 3.60 | .982 | -.411 | -.341 |

Table 16 shows that “Special banking is given to enhance the performance of the bank staff” is that the top stratified Responsiveness issue with an average of 3.92, “Reduce the waiting time” is that the second stratified Responsiveness issue with an average of 3.30 and “Offers a range of engaging loans and deposit schemes” is that the third stratified Responsiveness issue with a average of 2.99. Ranking for Accessibility issue in this study, Accessibility incorporates 2 factors that live Open branches within the prime locations so as to hide / attract the shoppers and supply free money practice. The table below shows the ranking for the things comprising the Accessibility that constitutes to items. Things were older on a five purpose Likert scale starting from ‘Highly Satisfied’ to ‘Highly Dissatisfied’. Ranking has been done supported the mean values.

| Responsiveness | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| Special banking is given to improve the performance of the bank staff | 3.92 | 1.091 | -1.133 | .882 |

| Reduce the waiting time | 3.30 | 1.017 | -.388 | .205 |

| Offers a variety of attractive loans and deposit schemes | 2.99 | .970 | .529 | -.353 |

Table 17 shows that “Open branches within the prime locations so as to hide / attract the customers” is that the top stratified Accessibility issue with a average of 4.11, “Provide free money consultancy” is that the second stratified Accessibility issue with a average of 2.86. Ranking for area issue in this study, area incorporates 2 factors that live Transparency in bankercustomer relations (make client feel user friendly) and also the car parking zone outside the Bank is giant enough. The table below shows the ranking for the things comprising the area that constitutes 2items. Things were older on a five purpose Likert scale starting from ‘Highly Satisfied’ to ‘Highly Dissatisfied’. Ranking has been done supported the mean values.

| Accessibility | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| Open branches in the prime locations in order to cover / attract the customers | 4.11 | 1.143 | -1.103 | -.035 |

| Provide free financial consultancy | 2.86 | 1.263 | .200 | -.938 |

Table 18 shows that “Transparency in banker-customer relations (make client feel user friendly)” is that the top stratified area issue with an average of 4.07, and “The car parking zone outside the Bank is giant enough” is that the second stratified area issue with an average of 3.26. Ranking for System issue in this study, System incorporates 2 factors that live the operating hours ought to be extremely convenient and versatile and change the documentation procedure / process the loans. The table below shows the ranking for things |the things} comprising the System that constitutes two items. Things were older on a five purpose Likert scale starting from ‘Highly Satisfied’ to ‘Highly Dissatisfied’. Ranking has been done supported the mean values.

| Space | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| Transparency in banker-customer relations (make customer feel user friendly) | 4.07 | .892 | -.820 | .025 |

| The parking space outside the Bank is large enough | 3.26 | 1.099 | -.160 | -.966 |

Table 19 shows that “The operating hours ought to be extremely convenient and flexible” is that the top stratified System issue with an average of three.54 and “Simplify the documentation procedure / process the loans” is that the second stratified System issue with a average of three.35.

| System | Mean | Std. Deviation | Skewness | Kurtosis |

|---|---|---|---|---|

| The working hours should be highly convenient and flexible | 3.54 | 1.298 | -.500 | -.791 |

| Simplify the documentation procedure / Processing the loans | 3.35 | 1.112 | -.181 | -.867 |

Now-days, banking sector acts because the backbone of contemporary business. Development of any country primarily depends upon the banking industry. A bank may be an institution that deals with deposits and advances and different connected services. It receives cash from people who need to avoid wasting within the sort of deposits and it lends cash to people who want it. The banking is one in all the foremost essential and necessary components of the human life. In current quicker modus vivendi peoples might not do correct transitions while not developing the correct bank network. The banking industry in India is dominated by nationalized banks. The performance of the banking sector is additional closely coupled to the economy than maybe that of the other sector. Supported the findings, this study offers some suggestions to the bankers so as to enhance the potency of the selling of the banking services.

1. Although the bankers area unit increasing the quantity of shoppers their rate of growth isn't satisfactory. So as to hide the population of the Taminadu, the bankers ought to take the required steps to extend the quantity of shoppers within the Tamilnadu.

2. Ancient banks have introduced mobile technology to enhance potency, maintain with digital trends, and satisfy client demands. Digital transformation within the monetary services sphere has created vital progress, with most mobile banking apps containing essential options.

3. However, contender banks create a big threat to ancient banks amid customers rising expectations for a direct and seamless user expertise. Within the digital age, customers can systematically worth convenience and digital potency over loyalty to long monetary establishments.

4. The study confirms that there are a unit variations within the opinions on the services. The bank marketers showed promotional message, policy and communications ought to be tailored to the assorted segments, specifically to the agriculturists.

5. Monetary sector reforms assisted spectacular development of the Indian banking system. However within the recent world competitive atmosphere, wherever it's serving to tremendous advancements with potency enhancements banking sector reforms in India area unit complete.

6. Delivery of services to a client by a bank in his workplace or home mechanically could also be termed as e-banking. The standard, vary and worth of those e-services decide a bank’s competitive position within the business.

7. The banks ought to rent the services of opposing Cybercrime skilled to avoid cybercrime to require the responsibility of customer’s transactions.

8. A Security set up ought to embody reviewing intrusion detection systems, maintaining well-trained workers to handle any laptop problems and shield the integrity of the information, and worker verification, together with background checks if necessary bank ought to upgrade the system and network and increase the national wide information measure the mainframe host capability, server and also the main frame storage capability to support the growing demand of shoppers.

9. Banks ought to make sure that on-line banking is safe and secure for monetary group action like as ancient banking. Structure bulletin boards might contain the subsequent like circulars, undesirable parties, hot list, bulletins, missing security things, confidential circulars on tried frauds.

10. Web banks ought to search for opportunities to lower the fees and transfer the price savings to customers.

11. The banker’s area unit suggested to produce ample workers and monetary help to modernize the operating conditions. The supply of progressive infrastructural facilities is that the ‘mantra’ for the success of the selling of the banking services. For that they need to produce additional infrastructure facilities temporary the operating conditions and also the appointment of technical workers all told the branches of banks within the Tamilnadu.

12. Nowadays, once any bank is willing to open a replacement branch or willing to shift the prevailing branch to new location, they realize ample area for the branch premises further as for automatic teller machines. This can be for the aim of serving to customers to urge immediate withdrawal of funds from the machines. Normally, they supply cash for cheques on top of the essential limit prescribed for withdrawal from automatic teller machines.

13. In cases wherever ATMs don't decide the cardboard, the officers managing money ought to remember enough to handle the matter. ATM machines ought to maintain and repaired straightaway. ATMs ought to be put in close to searching complexes, hospitals Malls, assembling centre’s, business institutions and straightforward accessibility from the road, not nearer to ponds, factories managing ignitable merchandise and decayable things.

14. Once a client goes to a bank he interacts with workers of that bank. For him, he's not interacting with an individual however with the bank. Therefore, the workers of the bank ought to be friendly, polite and trained enough to guide the client effectively.

15. The promotional measures like personal merchandising, loan melas, and advert through newspapers, co-operative bank workers, the posters and pamphlets could also be increased so as to retain existing customers and attract new customers within the state.

16. Regular feedbacks ought to be taken by the purchasers regarding the operating of the banks such feedback provides associate insight of shopper’s expectation from banks and provides scope for additional improvement.

17. The banks ought to correct usage of knowledge Technologies and fashionable amenities like ATM, Mobile Banking, SMS, banking, Electronic payment, money Dispensers, Real- Time Gross Settlement Systems (RTGS), National Electronic Fund Transfer (NEFT). Electronic Clearing Systems (ECS), Electronic Fund Transfer Systems, identification number based mostly Transactions for Magnetic cards- sensible cards, Credit cards and Debit cards. Offshore Banking/ Overseas Banking services.

In the days to come back, banks area unit expected to play a really necessary role within the economic development and also the rising market can offer business and selling opportunities to harness. As banking in India can become additional and additional information supported, capital can emerge because the finest assets of the banking industry. Ultimately banking is individuals and not simply figures. To conclude it all the banking sector in India is progressing with the multiplied growth in client base, because of the freshly improved and innovative facilities offered by banks. The economic process of the country is associate indicator for the expansion of the banking sector. The Indian economy is projected to grow at a rate of 5-6 % the country’s banking system is anticipated to reflects this growth. The worry for this lies within the capabilities of the bank of India as associate ready central administrative unit, whose policies have protected Indian banks from excessive investing and creating high risk investments. By the govt support and a careful re-evaluation of existing business ways will set the stage for Indian banks to become larger and stronger, thereby setting the stage for growth into a worldwide client base. The future success by any bank cannot be achieved while not the event of latest business concepts, innovative product associate services and intense specialize in client retention. Banks got to instill in their deoxyribonucleic acid the enablement of a positive and consistent client expertise which will remodel them into trustworthy advisers. Banking is one in all the various services within which client satisfaction has had associate ever-increasing importance within the corresponding analysis areas. This can be primarily as a result of the banking sector is changing into additional and additional competitive. Retail banks area unit following this strategy, in part, owing to the issue in differentiating supported the service providing. Client satisfaction in banking has not been neglected by researchers.

Accounting & Marketing received 487 citations as per Google Scholar report