Research - (2022) Volume 13, Issue 6

Received: 03-Jun-2022, Manuscript No. bej-22-65746;

Editor assigned: 05-Jun-2022, Pre QC No. P-65746;

Reviewed: 17-Jun-2022, QC No. Q-65746;

Revised: 23-Jun-2022, Manuscript No. R-65746;

Published:

27-Jun-2022

, DOI: 10.37421/2151-6219.2022.13.386

Citation: Bantu, Abebe Negesse and N.S Malik. “Effect of Socioeconomic

Factors on Loan Repayment Performance and Sustainability of Youth

Revolving Fund in Oromia Regional State, Ethiopia.” Bus Econ J 13 (2022): 386.

Copyright: © 2022 Bantu AN, et al. This is an open-access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

Ethiopian Youth Revolving Fund (YRF) loan was established with objective to provide financial and technical assistance to unemployed youths in alleviating their economic and social difficulties using the sustainably. However, the government and Oromia Credit and Saving Share Company (OCSSCo) reports showed that loan repayment was not performed as expected for the reason not yet been studied. Thus, the purpose of this study was to examine the effect of socio-economic factors on loan repayment performance and sustainability of YRF. The data was collected from 328 respondents from five clusters of Oromia Administrative zones. The descriptive and inferential statistics (chi-square test of association) were used to check the association of independent variables and their effect on dependent. The findings show the existence of peer pressure to use the fund for search for employment than facing hardship in creating job, poor business performance, loan diversion, and wrong choice of business types were affected YRF loan repayment performance at less than 5% level of significance. Finally, the government is recommended to work on creating awareness in public on creating own job, reconsider inclusion of entrepreneurship and business courses in the educational curriculum. OCSSCo should to provide adequate training and guidance to borrowers on fund utilization and management and arrange micro-insurance. Alternatively, the government should redesign the fund utilization by establishing businesses with the fund; employ the youths in it selling shares for each unemployed youth being employed in the business and finally handover the business to the youth after assuring financial viability.

Youth revolving fund • Socio-economic Factors • Loan diversion • Sustainability

Financial services provided by microfinance to the poor are among the poor are powerful tools to fight poverty. Access to a well-functioning financial system can allow individuals both economically and socially to integrate more successfully into the economy of countries and protect themselves against economic tremors. Access to government revolving funds helps the poor be involved in income-generating activities, which induce them to accumulate the capital needed for investment and improve their living standards [1-5].

In developing countries like Ethiopia, in most cases, poor people have no credit access from banks because of a lack of collateral to use as security. Microfinance provides poor people with financial services such as loans, savings, and micro-insurance on an individual or group basis to help them fill their financial problems [6]. On the other hand, the rise in youth unemployment is not proportional to the economic growth to generate job opportunities for all youth at the same time. In several countries, youth unemployment remains a major issue, especially in light of the current global financial and economic crisis. Currently, the issue of unemployed youth has become a serious agenda for most developing countries, specifically in sub-Saharan Africa (ILO, 2012).

The World Bank in “A 2015-baseline report of Solutions for Youth Employment (S4YE)” argued that today’s youth would not be able to escape poverty or address economic exclusion by 2030 if they do not have a means of employment [3]. A report by Ethiopia, “Voluntary National Review on Sustainable Development Goals (SDGs),” pointed out that a high unemployment rate needs special attention for increased and rigorous efforts to continuously build their capacities and systems that would eradicate poverty by 2030 [7,8].

In the struggle to enhance youth employability, eliminate poverty and accelerate development, many African countries (Botswana- National Youth Fund (NYF) in 2004, Mali- APEJ 2003, Tanzania - Tanzania Youth Development Fund (TYDF) in 1993/94, Kenya- National Enterprise Development Fund (NEDF) in 2006, South Africa- National Youth Development Agency Usombuvu Youth Fund in 2001, Namibia, and Tunisia- Youth Development Fund (YDF) in 2011, etc. have established Youth Revolving Funds in addition to the former efforts they made to help unemployed youth to start their businesses through MFIs (ILO, 2012). Ethiopia has also established the Youth Revolving Fund package as an additional special package for unemployed youth in response to common developmental goals by the Proclamation No. 995/2017, which amounted was $456 million USD (10 billion (ten billion) Ethiopia Birr). The objective of this is to provide youth with financial and technical assistance in alleviating their economic and social difficulties by engaging in group-based income-generating activities.

To ensure this objective, it is necessary to follow up and manage the implementation of the funds carefully for the sustainability of the fund and the success of youth employment objectives. However, the findings of many studies in different countries, specifically in underdeveloped and developing counties, showed that MFIs are suffering from loan defaults, both regular credit, and YRF credit, because of many reasons which may or may not be common to all countries [9-11]. The practical implementation of the YRF loan needs continuous follow-up and monitoring to ensure the fund's sustainability, as failure to manage the Youth Revolving Fund's sustainability may result in many negative consequences of youth unemployment.

When young people are not fully participated in the labor force, it will be a burden and risk for the government in the form of the increased cost of social safety nets, lost productivity, and ever-mounting social costs. When youth unemployment goes extreme, the consequences may expand to a similar situation to the Arab Spring (Towards Solutions for Youth Employment a 2015 Baseline Report). The finding of the study at Ambo town in Oromia, Ethiopia, on ‘consequences of youth unemployment’ depicted an increase in migrants, physical and sexual abuse, mental and psychological depression or hopelessness, drug addiction, illegal gambling, social unrest; community insecurity, crime, and national fragility are some of the consequences of youth unemployment [12]. These will hamper the country's national security and economic development and endanger the lives of unemployed youth.

Furthermore, there is a general potential fear that unless the concerns impacting Youth Revolving Fund repayments are addressed considerably, the program's sustainability will be elusive; as a result, youth employment will suffer, and the YRF's goals would be missed. The objective of this study was to examine the effect of socio-economic factors on loan repayment performance and sustainability Youth Revolving Fund in Oromia Regional State, Ethiopia.

The subsequent section of this paper is organized as follows: the next section, section 2, presents the literature review and conceptual framework of the study; section 3 shows the research method used; Section 4 presents the results and discussions and interpretations of the study and finally, section 5, focuses on presenting the conclusion and recommendations and presents implications and suggestion for further studies.

Theoretical review

The guiding principles of loan repayment state that banks and most financial institutions have used a credit policy to secure that their money is repaid, as stated in the loan operation agreements. According to Zena [13] banks and most financial institutions use some relevant loan operation principles as their guiding principles. This guiding principle focuses on borrowers' intention for the need loan, their repayment capacity, and personal character. Lenders should allow the borrowers to get for their needs, as loans are expected to be more valuable to meet investment needs.

The credit delivery system should create clear eligibility criteria that prioritize the most vulnerable households considering their repayment capacity. Borrowers' repayment capacity is the most important factor in determining their creditworthiness. To analyze the borrower's competence, lenders should look at the borrower's historical record (both personal and company profit), past success, and the borrower's reputation and attitude toward financial commitments. Lenders should constantly link credit to a borrower's positive personal characteristics, such as integrity, honesty, accountability, reliability, and sincerity.

In this study, there are certain guiding principles of loan repayment set by the government that are YRF loan specific for assuring the fund's repayment and sustainability. According to proclamation No. 995/2017, the beneficiaries of YRF loans in Ethiopia are expected to fulfill significant criteria such as certificate not employed and job seeker, being in the age range of 18 to 34 years of age, able to deposit(save) ten percent(10%) of the amount required for the proposed project, the interest rate charged on loan was 8%, the maximum ceiling payback period of five years, the borrower should have a good personal character from the community they lived in, and the business types they engaged.

Empirical review

Bukenya B, et al. [13] depicted how peer pressure negatively affected repayment performance, and the result showed that some youth convinced the group members and pressured them to share the money among themselves and do their business than doing the planned project. A study in Uganda by Bukenya B, et al. [13] also revealed that some group leaders develop a small clique and exploit the money to benefit themselves against the majority of group members and planned investment stated in the application for the youth loan funding which exposed the loan-to-loan losses.

The study on “loan default and performance of the Youth Enterprise Development Fund of Dagoretti” in Kenya found that loan diversion was among the factors that negatively influenced loan repayment performances and impaired sustainability [14,15]. Another study in Malaysia also revealed a negative relationship between diversion of funds and loan repayment in which many borrowers used the fund for unintended (non-investment) purposes, resulting in an increased probability of the loan default [16,17] also identified that variables like repayment schedule and loan diversion for celebrations of social ceremonies, other sources of income, and external economic shock significantly and adversely affected the loan repayment performance.

The diversion of loans for social occasions, such as marriages, circumcision, and the funeral of a family member or close relative that require financial resources above what the borrowers can afford and were obliged to redirect funds for social ceremony celebrations and forced to default the loan, was discovered in research by Gebeyehu and Million as among factors that increase loan defaults. The study by Abera and Asfaw also showed that variables including family size, the distance of the loaning institution from the borrower's house, and revenue gained from projects financed by the loan have a substantial impact on borrowers' loan repayment performance [18].

The nature of business operations financed by loans significantly impacts loan repayment performances. The study's findings in Malaysia on determinants of microcredit loan repayment problems disclosed that borrowers who were interested in agricultural operations had difficulty repaying their loans on time. As per the finding, the main reason for loan default was the nature of their businesses’ irregular revenue caused by drought or flood, where there was no micro-insurance policy, especially weather insurance for borrowers. The study in Kenya on “loan default and performance of the Youth Enterprise Development Fund” discovered that most defaulted groups were those whose businesses failed because of the wrong choice of the businesses financed by loans [15]. Another study in Kenya also showed that the manufacturing sector was the defaulted sector, followed by the service industry. Whereas; agriculture and trade sectors were ranked among the minor loan repayment defaulted sectors. According to the finding, poor business proceeds, investments that took a long time to mature (business life), and a lack of continuity in groups were all blamed for the low repayment [19,20].

The result of the study by Jote GG [20] using a binomial logistic regression model revealed a favorable relationship between the borrower's residence and loan repayment MFIs. The findings concluded that as closer a borrower is to the institution, the better (becomes closer to the institution), and so does their ability to repay their loan. Abera and Asfaw, using the ‘Tobit model’, also showed that the further distance between the lender’s office and the borrowers' residence posed a substantial harmful effect on the borrowers' ability to repay their loans. In contrast to this, borrowers who live near the lender's office are more likely to repay their debts. The study findings on “factors affecting loan repayment performance of smallholder farmers in East Hararghe”, Ethiopia, investigated that the average revenue earned by a borrower from crops and livestock during the production directly affected the loan repayment performances. The finding showed that non-defaulters obtained more cash from crops, livestock, and additional income from off-farm activities than defaulters [21,18].

Conceptual framework

Considering the various socioeconomic factors related to variables that could affect loan repayment performances and the sustainability of YRF in Oromia/ Ethiopia, the researcher developed the following conceptual framework. The conceptual model is used to assess overall factors related to loan repayment performance and sustainability of YRF, such as Youth perception/mindset, peer pressure, belief in society on creating own job, loan diversion, poor business performances, and predominant shocks in the economy as indicated in Figure 1.

Figure 1. Conceptual framework of the study (Source: Researcher’s own development (2021)).

Descriptions of the study area

The research was conducted in Ethiopia's Oromia Regional State, located in Africa's horn. Ethiopia is organized into eleven regional states and administrative councils. Oromia (Oromiyaa) is the largest region in geographical area and population and the homeland Oromo people. It is situated in the heart of the country, surrounding Finfinne, also called Addis Ababa (the capital city of Oromia and Ethiopia), in all directions. Currently, the state has 21 administrative zones and over 300 districts, all of which have a pleasant climate for life and good fertile land for investment and development. Oromia's population was estimated to be about thirty-eight million in mid-2018, and its land area is about 535,690 square kilometers (CSA, 2020). Figure 2 shows the map of Oromia Regional State in Ethiopia in East Africa.

Figure 2. Map of Oromia Regional State (Source: http://www.ethiodemographyandhealth.org/(2021)).

Sampling techniques and procedures

From the total population of 29,942 YRF loan beneficiary groups and loan officers in the region, a representative sample of 380 was selected using Kothari formula at 95% level of confidence and a 5% confidence interval to enhance the reliability of the findings.

Where;

N = Total population of the study

z = 1.96 (as per table of area under normal curve for the given confidence level of 95%).

P = the proportion of participation or perception,

q = the proportion that may not include and

e = the error term

Methods data collection

The representative sample size was determined using a multi-stage sampling method. Stage I, 20 Oromia zones, were divided into five clusters based on geography and business activities. In a sampling design stage II, sample respondents were proportionally allocated to the percentage of the total population of the nine (09) purposively selected zones. Finally, 380 respondents were selected from 14,183 beneficiary groups in the selected cluster zones (353 sample beneficiary groups through simple random sampling techniques and 27 loan officers).

Methods of data analysis

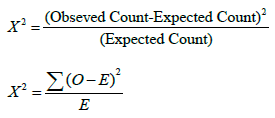

Structured questionnaires, semi-structured interviews, and Focus Group Discussions (FGD) were used to collect primary data from the selected sample size. The masses data or information was summarize used descriptive statistics such as frequency and percentage and The study used the chi-square test to check for a statistically significant relationship among the independent variables and the respective dependent (outcome) variables and the formula for chi-square as per.

Where,

χ2 = The value of chi square

O = The observed value

E = The expected value

Σ (O – E)2 = all the values of (O – E) squared then added together

The response rate

A total of 380 sample respondents were used for this study by dividing them into two response categories (353 sample respondents were selected to respond to questionnaires, and 27 respondents were addressed through the interview). From 353 questionnaires distributed to respondents, 85% of questionnaires were correctly filled, collected, and used for this study analysis. All twenty-seven (27) respondents were selected for an interview well addressed, and their responses were included in this analysis. The overall response rate for this study was about to 86% of the target sample respondents. According to Draugalis, JR, et al. [21] JoLaine, RD, et al. [22] and Melese M, et al. [23] 50%-60% or above response rate is ideal and sufficient for research. As a result, the response rate for this survey (86%) was excellent, as it was higher than the optimal standard.

Chi-square test results

The objective of this study was to determine the effect of socio-economic factors on loan repayment performances and the sustainability of YRF in Oromia, Ethiopia, and the result of the respondents' responses was summarized in Table 1. The result in Table 1 indicates that there is a significant relationship between socioeconomic factors and YRF loan repayment performances and its sustainability. Almost all of the sample respondents (95% and 94%) reported that peer pressure influenced the borrowers to use the fund to search for governments or non-governmental organizations (NGO) employment than facing hardship in creating their businesses (jobs), and prevailing shocks in the economy were the problems that cause YRF loan to default respectively. This implies that because of peer pressure fund was diverted to unplanned expenditure than used to finance the proposed project, which may affect YRF loan repayment performances.

| Assessment Tools/Items | Likert Scales | χ2 | P-values | ||

|---|---|---|---|---|---|

| D | N | A | |||

| № (%) | № (%) | № (%) | |||

| Peer pressure to use the fund to search for government employment than facing hardship in creating own businesses (jobs). | 7 (2) | 8 (3) | 286 (95) | 9.691 | 0.008 |

| The belief in society to be employed in other organizations than creating own job is the main cause for loan diversion. | - | 36 (12) | 265 (88) | 33.704 | 0.000 |

| Income from the type of business financed by the loan has a significant effect on Youth Revolving Fund loan repayments. | 6 (2) | 32 (11) | 263 (87) | 28.062 | 0.000 |

| Loan diversion to unplanned expenditure is the main caused the loan default. | 9 (3) | 54 (18) | 238 (79) | 31.575 | 0.000 |

| Youths use income from investments financed by fund loans for daily consumption to sustain their lives. | 9 (3) | 35 (12) | 257 (85) | 18.986 | 0.000 |

| Poor business performance is the cause for loan default. | 20 (7) | 40 (13) | 241 (80) | 40.582 | 0.000 |

| Predominant shocks in the economy causes of loan default. | - | 19 (6) | 282 (94) | 0.570 | 0.450 |

| The time of maturity of investment (revenue cycle) determines the loan repayment status of the groups | 12 (4) | 57 (19) | 232 (77) | 41.566 | - |

The result showed that a large number of respondents (88%, 87%, and 80%) indicated that the belief in society to be employed in other organization than creating own job was the main cause for loan diversion, income from the type of business financed by the loan has a significant effect on YRF loan repayments and poor business performance was the man cause for loan default while others respectively. This shows that youths divert the loan to search for employment than creating their job because of the belief in society and the income from the business specifically when borrowers incur losses they make low repayment or ban the repayment has a significant effect on YRF loan repayment performance and its sustainability. The result (Table 1) indicated that there is a significant relationship between loan repayment performance and loan diversion. The majority of the respondents (79%) reported that the loan diversion for unplanned expenditures (marriage, funeral, and other social ceremonies) was the main cause of loan default. This shows that many economic problems enforce the borrower to diverse the fund to other expenditures negatively affecting the loan repayment.

Another economic factor that has a significant relationship with loan repayment performance is the use of the fund for daily consumption. The result (Table 1) showed that 85% and 77% of the sample respondents responded youths use income from investments financed by fund loans for daily consumption to sustain their lives and the time of maturity of investment (revenue cycle) determines the loan repayment status of the groups respectively. This shows that since youth have no other sources of income they prefer to use income from an investment to sustain their families’ life which directly negatively influence the loan repayment performance. On the other hand, the loan repayment performances of borrowers with a short revenue cycle will differ from those with a longer (seasonal) revenue cycle.

The Chi-square (χ2) test shows that there is a statistically significant relationship between peer pressure, the belief in society, poor business performance, use of income for daily consumption, loan diversion, income from the type of business financed by the loan, and time of maturity of investment (revenue cycle) and the YRF loan offices and YRF loan repayment performances and its sustainability at less than 1% level of probability. However, the Chi-square (χ2) test shows that there was no statistically significant relation between prevailing shocks in the economy and YRF loan repayment performances (P-value= 0.45 and χ2= 0.576) (Table 1).

The peer pressure to use the fund to search for government employment than facing hardship in creating job and earning income from the type of business financed by the loan facing hardship in creating own businesses. This finding is linked with the result of the study by Bukenya B, et al. [13] that showed that some youths convinced the group members and pressurizing other members to share the money among them and do their business than doing the planned project. On the other hand, the current study is supported by the finding of Melese who identified that loan repayment performance was significantly and adversely affected by variables like poor business performance or business losses, unsuitable repayment schedule, and loan diversion for celebrations of social ceremonies, holding the fund fearing the risk of business failure and the time of maturity of the investment [24,25].

The finding shows that the time of maturity of investment (revenue cycle) of borrowers’ business determines their loan repayment status (borrowers with a longer revenue cycle were committed the difficulty to perform repayment for a short repayment schedule). The current study result is in line with Mokhtar SH, et al. [5], who noted that since the weekly loan repayment method is challenging for persons with little income, a longer payment period is preferred over a short one. However, the current finding is contradicted by Muthoni, who claimed that loan repayment duration was shown to be relevant in MFI loan repayment, and also argued that the longer loan period may result in a greater risk of default in MFIs. On the other hand, the current study is linked with Jote GG [20] and Abera and Asfaw, which found that the borrower's residence's proximity to lending institutions, as well as revenue from activities financed by a loan, were key determinants impacting borrowers' loan repayment performance. In addition, the current finding is supported by Aberi and Jagongo, which indicated that most defaulted groups were those whose businesses failed because of the wrong choice of the businesses financed by the loan [25].

The current study showed that income from the type of business financed by the loan has a significant effect on Youth Revolving Fund loan repayments and it is consistent with the findings of Abebe which revealed that loan repayment has a significant relationship with the nature of and type of business the borrowers engaged. On the other hand, the current result shows that YRF loan repayment performance was negatively affected as some youths used income from investments financed by fund loans for daily consumption to sustain their lives. This result is supported by the finding of Warue, Ojiako and Ogbukwa and Arene who found that borrowers’ income, family size, and family living expenses were among some factors that influenced their loan repayment capacities.

The current study shows that prevailing shocks in the economy were not indicated as the main causes of loan default. This result is in agreement with the finding of Constantinou & Arvind, revealed that microfinance is primarily informal and directed at non-global entrepreneurial ventures (except for those engaged in cash crops and tourism-related micro-businesses), which implies that the impact of global economic events would not be significant. However, it contradicted the finding of the study by Njeru, and Waweru and Kalani, which revealed that a rising scope of loan default is associated with adverse macroeconomic shocks/ economic downturn contributes to reduce credit economic power to pay debts.

Status youth revolving fund of loan utilization

The finding of the study indicated 59% of respondents diverted the loan for an unintended purpose (expenditure), whereas, the remaining 44% of them used the fund for the proposed projects. Figure 3 shows the proportion of the respondents that diverted and not diverted the fund loan to unintended use.

Figure 3. Status Youth Revolving Fund Loan Diversion (Source: Survey Data (2021)).

Causes of youth revolving fund loan diversion

The result (Figure 4) showed that respondents have different reasons for diverting the YRF loan for an unintended purpose. A large number of respondents (24% and 23%) argued that the loan they received was insufficient for the intended purpose and excessive level of snowballing perception about YRF loans as grants that will not be paid back respectively. 16% of the respondents reported that youth used the fund for consumption to sustain their lives as they have no other source of income; 14% of them used the fund to cover expenditures for circumstances at disposal compels (marriage, funeral, etc.); 11% because of fear of the risk of business failure; 7% because of pressure from family to seek employment than creating own job and literacy and 5% because of low level of education.

Figure 4. Causes of YRF Diversion (Source: Survey Data (2021)).

This result is consistent with the result of the study in Uganda by Bukenya B, et al. [13], who found why youth divert the revolving fund to consumption expenditure to meet their basic needs as they have no other sources of income to sustain their life than doing the planned investment projects. The current study result is similar to the result from Malaysia by Murthy and Mariadas, which also concluded the negative relationship between loan diversion and loan repayment performances. The findings of the study by Aberi and Jagongo also indicated the main issues that led to the youths diverting borrowed funds were poor business performance and illiteracy (Figure 4).

The current study found the existence of peer pressure to use the fund for search employment than facing hardship in creating a job. As a result, some youths convince and pressurize other group members to share the money among them and do their individual business than doing the planned project. Other economic factors that affected loan repayment performances were poor business performance or business losses, unsuitable repayment schedule, loan diversion, holding the fund fearing the risk of business failure, the time of maturity of the investment, distance of the borrower’s residence from the lending institutions, wrong choices of type of the businesses financed by loan and loan diversion to unplanned expenditure because of different reasons were significant factors that negatively affected the loan repayment performance and sustainability of YRF.

Based on the above findings, the current study makes recommendations to concerned bodies involved in the Youth Revolving Fund loan management to enhance repayment performance and sustainability.

• Government should reconsider inclusion of entrepreneurship and business courses in the educational curriculum just similar to civic and ethical education to induce business concepts and benefits of creating own jobs in different levels of education than teaching to uploading merely academic knowledge.

• OCSSCo should work to help borrowers on choosing the right business and provide continuous guidance to enhance borrowers’ business performances and also facilitate micro-insurance policies to help them safeguard from unexpected business losses. Moreover, pre-fund release training should be given to qualified candidates as per regulation for not less than a month than giving very general three days of training and release the fund for beneficiaries.

• Another better alternative to solve socio-economic problems is the government should redesign the utilization of the fund by establishing businesses with the fund, employing the youths in the established business selling shares for each and operating the business giving a majority of the management to them with strict control on the performance and status. Then, the government should gradually turn the key to the youth group and withdraw totally with remote supervision after assuring proper management and the smooth operation of the business.

The current study has some limitations that were not covered in this study but can be an opportunity for future research. Accordingly, the following is area of recommendation for further studies:

• There is a need to do a comparative study on loan performance and the sustainability of YRF urban and rural beneficiaries.

The first author is grateful to Ministry of Education and Oromia State University (Ethiopia) for sponsoring me the fellowship program and Guru Jambheshwar University of Science and Technology (India) for hosting me study my Ph.D.

The authors have no financial and non-financial conflict regarding this manuscript and we confirm that it is our responsibility for any issue with regards.

Google Scholar, Crossref, Indexed at

Google Scholar, Crossref, Indexed at

Google Scholar, Crossref, Indexed at

Google Scholar, Crossref, Indexed at

Google Scholar, Crossref, Indexed at

Google Scholar, Crossref, Indexed at

Google Scholar, Crossref, Indexed at

Google Scholar, Crossref, Indexed at

Google Scholar, Crossref, Indexed at

Google Scholar, Crossref, Indexed at

Google Scholar, Crossref, Indexed at

Business and Economics Journal received 6451 citations as per Google Scholar report