Research Article - (2021) Volume 0, Issue 0

Received: 25-Mar-2021

Published:

15-Apr-2021

, DOI: 10.37421/2151-6219.2021.s2.002

Citation: Soukaina, Khadhraoui and Sami Hammami. "The Dynamic

Links between Public Debt, Unemployment, and Budget Deficit in the MENA

Countries and Eurozone during 1990 to 2016 Fresh Evidence from Simultaneous Equation Models " Bus Econ J 12 (2021)S2:002.

Copyright: © 2021 Soukaina K et al. This is an open-access article distributed

under the terms of the Creative Commons Attribution License, which permits

unrestricted use, distribution, and reproduction in any medium, provided the

original author and source are credited.

This study aims at examining the interactions between three macroeconomic variables, namely: public debt, unemployment and budget deficit. We have assumed that the increase in unemployment is caused by the worsening of the budget deficit and the increase in public debt. To test this hypothesis, we have used a system of simultaneous equations in macroeconomic data from 1990 to 2016 in six countries of the Euro zone countries such as (France, Spain, Portugal, Greece, Ireland and Cyprus) as well as five countries of the MENA countries namely (Tunisia, Algeria, Morocco, Egypt and Jordan).

All the variables were found to be stationary based on recent panel unit root tests. On fully applying both static (, FE, and RE) and dynamic (system GMM) panel data approaches, it was found that confirm that the results of the model estimation for the six countries of the Euro zone approve that there is a two-way relationship there is a two-way relationship between unemployment and debt. Similarly, there is a two-way relationship between the budget deficit and unemployment. At another level, we note a unidirectional relationship from budget deficit to public debt. However, for the five countries of the MENA countries we have found a unidirectional relation going from public debt to unemployment, a twin directional relation between deficit and unemployment and a unidirectional relation going from debt to the deficit.

Budget deficit • Public debt • Unemployment • MENA • Eurozone • Simultaneous equations

The problem of unemployment has become gradually more important in modern economic research, making it a central argument of contemporary public policy, particularly during the last few decades when the economic context of all developing and developed countries has been marked by massive indebtedness, deterioration in the pace of economic growth, labor market rigidities and rising unemployment rates. As a result, after the 2007 crisis, the European Union and the MENA region became a zone of mass unemployment. In 2011, the outbreak of the Arab Spring in 2011 reinforced the swelling of the unemployment problem, particularly in Tunisia and Egypt which had reached 16.7% and 19.5%. As for Morocco, with an unemployment rate of 9.4%, it was in a better position than its neighbors, due to the reforms it has undertaken and the new constitution signed in 2011. According to the statistics published by the World Bank we have noticed that during the period from 1990 to 2016 the unemployment rate on average was much higher, especially in Greece and Spain and lower in Portugal, Cyprus and Ireland (8%, 8.25%, and 9.67% respectively). The wide disparities in unemployment rates observed in the region are not only explained by divergences in the employment growth, but are also largely the result of activity patterns within countries in a context of integrated labor markets. Employment has followed very different trajectories in these countries, and rising unemployment has affected populations unevenly.

To highlight the main objective of this research, this article addresses the problem of rising unemployment rates. Therefore, we have assumed that the increase in unemployment is caused by the worsening of the budget deficit and the increase in public debt. To test this hypothesis, we used a system of simultaneous equations with panel data from 1990 to 2016 on a set of euro zone countries such as (France, Spain, Portugal, Greece, Ireland, and Cyprus) and for a group of MENA countries (Tunisia, Algeria, Morocco, Egypt, and Jordan). The estimation of the model will include the analysis of the data to identify the essential characteristics of the variables. The estimation of the model will include the analysis of the data to identify the essential characteristics of the variables and will continue with the study of the stationary of all the variables of the model. In order to arrive at the results, a Hausman specification test will be applied to determine which of the regressions (fixed effects or random effects) is most appropriate. Then, a heteroskedasticity test will be done to verify if the variables are homoscedastic. Afterwards, the model will be estimated either by fixed effects or random effects é. Finally, the simultaneous equation method will be used to verify the relationship between the variables of research interest.

The budget deficit has been the economic challenge of many countries in recent decades. This scourge is widely perceived in developing countries because they are deprived of an effective private sector. This leads to the expansion of government activities and the increase in the economic share of the state in these countries, so that a considerable part of the total demand is allocated to public spending and investment. On the revenue side, the government cannot cover its huge expenditures with additional revenue. The result of this process in these countries is nothing more than a permanent budget deficit. If the government relies on banking resources to finance the budget deficit, this can lead to economic inflation, such that the internal (domestic) imbalance would also affect the external economic sector, as an increase in public spending initially leads to an increase in total demand. Indeed, an increase in public spending on the total supply side may not be translated into supply growth due to structural economic troubles and the lack of attractiveness of total supply. The end result of these factors is the emergence of inflation in the economy. In this situation, imports are increasing and exports are declining. Thus, the unbalanced state budget transferred to the external part leads to a current account deficit in these countries. In one study, Afonso and Tovar Jalles examined the effect of the budget deficit (from the point of view of public debt) and the total effectiveness of production factors on the economic growth of 155 selected countries worldwide. The results of the research show that government debts have a significant negative effect on economic growth, while the total effectiveness of production factors has a considerable positive effect. Marashdeh and Salman Saleh, in a research examining the government's budget deficit and trade deficit, concluded that the trade deficit in Lebanon had a long-term effect on the budget deficit. Salman Saleh also considers that there is a positive and significant relationship between the trade deficit and the budget deficit in Lebanon. According to him, policies to reduce the trade deficit are effective in reducing the budget deficit in Lebanon. Vito Tanzi, in finding the answer to the question of whether the historic and unprecedented budget deficit that the United States experienced in 1980-84 can be real as one of the factors explaining the high interest rate, thinks that the interest rate is indeed positively linked to the budget deficit and the level of public debt; furthermore, given the constant conditions, the interest rate was increased by the increase in the budget deficit. In his view, the major increase in real interest rates during the period 1981-1984 was independent of financial variables and economic conditions such as the revision of financial market rules, migration, and change in monetary policies and, more importantly, changes in tax regulations played a key role in changing interest rates during that period. Several perspectives have been formed in the area of the budget deficit influencing economic growth and the efficiency of factors of production; however, the views are inconsistent in many respects [1-3].

Keynesian theory

The Keynesian macroeconomics theory states that the budget deficit should be applied as a means of improving economic conditions and, as an appropriate policy, should allow politicians to maximize social welfare. Therefore, in Keynesian perspective, governments address the variables of production growth and unemployment; it also follows the policy that minimizes the difference between actual unemployment and the normal level of unemployment. Subsequently, Keynesian theory predicts that budget deficit is negatively correlated with unemployment, while the budget deficit is positively related with economy’s real growth rate. Therefore, the economic growth rate variable is introduced as changes in gross domestic product (GDP) growth to examine this theory. The variable coefficient demonstrates that fiscal policies should be employed in a way that leads an improved economic production level [4].

Ricardian equivalence

This theory created based on the two assumptions of rational expectations that households are prospective and households’ visions until taxation. As taxes reduced and budget deficit supplied through borrowing, the government would have no choice of expanding taxes in the future in order to repay the debts and interests. According to this perspective, Ricardo considers that people found out by experience that increased government bond as a result of diminished taxes offers temporary revenue for the individual at the present time. Next augmented government debt, these consumers save more to provide higher tax paying in the future; thus, increased public saving offers more credit to families and economic enterprises. As a result, amplified loan demand by government would be compromised by higher saving; so, the interest rate remains unchanged, and the decrease in taxes may not lead to permanent revenue, households save temporary inco diminished me with no change in order to pay the future tax liabilities, in term on savings, caused by current tax cuts. So, any reduction in current tax must be consistent with increase in future taxes; further, the augmenting of private saving would totally compromise reduction in public sector savings. National saving and thus the interest rate remain unchanged, which consequently leads to unchanged private sector investment. In other word, the effects of tax cut resulted from budget deficit cause properly increasing of private sector saving; according to logical consumption by consumers and concerning permanent consuming of consumers, no change in national savings may lead to no change in interest rate. Ricardo believed that budget deficit increased due to increasing costs of government, which may be paid now or in a later time. Consequently, tax cuts generated by the policy of budget deficit have no effect on consumption and saving; it employs no change on other economic variables including economic growth through this.

The relationship between public debt and growth

The issue of the relationship between public debt and economic growth has shown in the literature that the level of public debt plays a very important role in its impact on economic growth. Most of the work on this topic indicates that high levels of public debt have a negative effect on long-term growth. One of the most influential analyses of this issue is the work of Reinhart and Rogoff. They suggest the possibility of a non-linear correlation between real GDP growth and the debt-to-GDP ratio. They show that real GDP growth tends to decline if the debt-to-GDP ratio is very high. However, they add that there is no significant relationship between the accumulation of public debt and economic growth if the debt-to GDP ratio is low. Herndon has criticized the work of Reinhart and Rogoff. The authors re-did the work and found that errors in coding, selective exclusion of available data and unconventional weighting of summary statistics lead to serious errors that inaccurately reflect the relationship between public debt and GDP growth. In 20 advanced post-war economies, they estimated that when correctly calculated, the average real GDP growth rate in countries with a public debt ratio of more than 90 per cent has a factual effect of 2.2 per cent, rather than -0.1 per cent as published by Reinhart and Rogoff. For them, the relationship between public debt and GDP growth varies considerably depending on the period and the country. However, many empirical papers published following the work of Reinhart and Rogoff found similar conclusions to in original paper. They find that the relationship between debt and growth is non-linear and characterized by the presence of a threshold at which economic growth starts to slow down. For example, Kumar and Woo analyzed the impact of public debt on long-term economic growth. This analysis is based on a panel of 38 advanced and emerging countries over the period 1970-2007. They have validated that the debt threshold is 90%. ChecheritaWestphal and Rother studied the impact of public debt on the growth of GDP per capita in 12 countries of the euro area over the period 1970-2010. They conclude that there is a non-linear relationship between debt and growth when the debt/GDP ratio is 90-100%. They also analyses the channels through which public debt is likely to affect economic growth. The channels through which public debt is found to have a non-linear impact on the rate of economic growth are private savings, public investment and total factor productivity. Baum on a panel of 12 euro area countries for the period 1990- 2010 also validated that the threshold debt is 90%. Swamy has shown that the effect of debt on growth differs across countries and depends mainly on debt regimes and other important macroeconomic variable such as inflation, trade openness, government spending on consumption and foreign direct investment. Chudik have shown that the effects of public debt on growth vary across countries, depending on factors and institutions within each country [5-9].

Eberhardt and Presbitero suggested that the debt-growth relationship differs across countries. In addition to this work, which focuses on the level of public debt, there is work that has studied the impact of the public debt trajectory on economic growth. Using data on a sample of 40 countries over the period 1965- 2010, Chudik concluded that there are negative long-term effects of public debt and inflation on the economic growth. If debt relative to GDP is high and the increase is permanent, there will be negative effects on economic growth. But if the increase is temporary, then there will be no effect on long-term growth because the debt-to-GDP ratio is reduced to its normal level. They also conclude that the debt path may have more important consequences for economic growth than the level of debt itself. Pescatori focus on the long-term relationship between the stock of current debt relative to GDP and GDP growth in the coming years. They find that there is no net threshold that seriously hampers growth in the medium term and that the debt trajectory has more important consequences for economic growth than the level of debt itself. They also find evidence that higher debt appears to be associated with a more volatile growth that may nevertheless be detrimental to economic welfare. Panizza and Presbitero reviewed the theoretical and empirical literature that studies the relationship between public debt and economic growth in advanced economies. They found that there is no paper that can make a strong case for a causal relationship ranging from debt to economic growth and that the case for a causal effect ranging from high debt to low growth has yet to be made. They also found that the presence of thresholds for a not monotonous debt-growth relationship is not robust to small changes in data coverage and empirical techniques. Thomas Herndon, Michael Ash and Robert Pollin revealed methodological errors in the study by Reinhart and Rogoff Markus has published a working paper for the International Monetary Fund in which he finds that while there is a debt threshold above which public debt is harmful to growth, it is not common to all countries and is not constant over time, leading them to reject the idea that the same economic policy is not necessary applicable to all countries, let alone at the same time. In a new IMF publication, Andrea Pescatori, Damiano Sandri and John Simon used a new econometric method to take into account reverse causality, i.e. the impact of economic growth on public debt. The authors find no empirical evidence for the existence of a threshold of public debt at which medium-term growth prospects are affected. On the contrary, the medium-term association between public debt and growth weakens for high levels of debt. A study by Igberi christiana Ogonna, Odo Stephen Idenyi,Anoke Charity lfeyinwa and Nwachukwu gabriel therefore concluded that public borrowing in Nigeria has not created the desired impact in the economy. Consequently, the increase in public debt has not reduced unemployment. Furthermore, the rapid increase in debt service obligations is an obstacle to the implementation of new development-oriented projects, thus worsening the unemployment situation, as part of the revenue for this purpose is earmarked for servicing previous debts. It is pertinent to note that this obvious problem is attributed to the level of corruption prevailing in the economy, the distribution of public expenditure and the diversion of borrowed funds to unproductive or non-investment oriented projects which should in turn create employment. Numerous studies have then examined the link between public debt and economic activity. For example, Carmen Reinhart and Kenneth Rogoff have suggested that high public debt is associated with lower activity, but the direction of causality is unclear. However, as Ugo Panizza and Andrea Presbitero point out, it may simply be low activity that tends to push public debt to higher levels. Alan Auerbach and Yuriy Gorodnichenko have studied a sample of about 20 developed countries and confirm that stimulus through public spending increases stimulates activity and that the size of the public spending multiplier depends on the position in the cycle : a stimulus will stimulate economy’s activity more when the economy is depressed than when it is expanded. Moreover, they find that public expenditure shocks do not lead to sustained increases in public debt-to-GDP ratios or financing costs for fiscal authorities, especially in periods of economic weakness. Indeed, stimulus packages in depressed economies not only stimulate output, but also improve the fiscal sustainability, according to the various indicators that Auerbach and Gorodnichenko study. In short, it is unlikely that a government will see its interest rates or debt ratio rise sharply when it increases spending to cope with a recession; even if it’s public debt is initially high. Yi Huang, Ugo Panizza and Richard Varghese analysed data for a sample of nearly 550,000 companies in 69 countries, both developed and emerging countries, over the period 1998 to 2014. They found a negative correlation between public debt and business investment: high levels of public debt are associated with lower private investment and with a higher sensitivity of investment to internally generated funds. activity, thus incurring debt. Huang and his co-authors believe, however, that the causality is This correlation could reflect a Keynesian causal ranging from the low investment in public debt (or rather, the action of a third variable, namely low activity): when companies invest les, which is likely to be the case during a recession, the government will tend to stimulate in the opposite direction [10-15].

The relationship between budget deficit and economic growth

The explanations of the impact of budget deficits on the economy vary across different schools of thought. The neoclassical theory illustrates an inverse relationship between economic growth and budget deficit, because persistent deficits crowd out private investment. Cebula investigates the impact of U.S. budget deficits on the real GDP growth over the period 1955- 1992. However, the Keynesian school views that a budget deficit will achieve a national income improvement and need not crowd out private investment, if the resources in the economy are initially under-employed. In contrast, the Ricardian school views a budget deficit as merely postponing tax, and having no real effect. The Ricardian argument is built on the understanding that a lower tax rate and a budget deficit require higher taxes in future. The study of Cebula indicates that federal budget deficits reduce the rate of economic growth. Siddiqui and Malik state that the impact of the budget deficit to GDP ratio is expected to negatively crowd out public saving [16,17].

The relationship between debt and unemployment

In the study by Fedeli and Forte covering 19 groups of Organisation for Economic Co-operation and Development (OECD) countries and 13 groups of EU-OECD countries for the period 1981-2009. Another research that would be taken into account is that conducted by the Kurecic and Kokotovic, a linear regression conducted for five of the EU15 countries concerning the effect of public debt on unemployment revealed a statistically significant correlation between the variables. At the same time, the study pointed out that there is a strong causality between public debt and unemployment; for example, unemployment would increase by about 2.7% if public debt increases similar to those of 2012 and 2013 in Portugal, Greece, Ireland and Italy. This research on the relationship between public debt and unemployment has defined the budget deficit as a negative determinant of unemployment. It is also worth mentioning the study by Korol and Cerkas on Greece, whose conclusion argues that a 1% increase in public debt increases the unemployment rate by 0.46%. Oganna analyzed the Nigerian economy between 1980 and 2015 and argued that a 1% increase in public debt would lead to a 1.6% increase in unemployment due to the long-term relationship between the two variables. Last but not least, Jimenez and Mishra confirmed the distorting effect of the increase in public debt on unemployment through their academic work on the influence of the increase in public debt on the demand for labor in the United States for the period 1980-2008. The list of studies on the relationship between public debt and unemployment can be extended; it should be noted, however, that there is a large body of valuable work studying the relationship between external debt and unemployment. The study by Kokotovic can be considered pioneering in this respect. The study's sample consists of Spain, Greece, and Croatia, which has the highest levels of youth unemployment, followed by Germany, Denmark, and the Czech Republic, which have the lowest youth unemployment rate in the EU. The results of the estimation of the Autoregressive Distributed Lag (ARDL) show that youth unemployment is more affected by public debt than total unemployment in Croatia and Spain. The author stressed that new economic measures should be implemented to combat youth unemployment in those EU countries that are still suffering the destructive effects of the 2008 global financial crisis [18-20].

Data

Our investigation is based on annual data provided by several international institutions. We use data for the six euro zone countries (Spain-France- PortugalCyprus-Ireland-Greece) and five the MENA region countries (Tunisia, Algeria, Morocco, Egypt, Jordan). We have used annual data from international institutions in our empirical framework (IMF and World Bank, OECD, INSEE, Eurostat) which were mobilized to build a database covering the period 1990- 2016, i.e. 26 observations.

Model specification

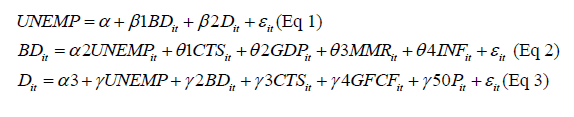

Modeling operates in three phases: design, i.e. writing or specifying the model; model estimating equations, and the use of appropriate techniques. To ensure the interrelationships between the three variables in our study (public debt, budget deficit, unemployment,) we have used a system of equations that recognizes the endogeneity of the explanatory variables under study. Our model consists of the three following equations:

With:n UEMPit, represents respectively, unemployment rate, public debt and budget deficit. CTS: the sustainable primary balance threshold calculated from the accounting approach of a country i at a time t. α1, α2 and α3 are the parameters to be estimated UNEMP (it-1) DP (it-1) and BD (it-1) represent the delayed dependent variables.

Dit: The euro zone public debt ratio as a % of GDP

BDit: The budget deficit rate as a % of GDP

UNEMPit: The unemployment rate

GDPit: The current GDP growth rate

INFit: The inflation rate

OPit: Opening Rate

MMRit: Money Market Rate

GFCFit: Gross fixed capital formation

CTSit: Indicates the critical threshold of sustainability

Descriptive statistics

The following is a sum up description of the data from the research. Thus, the table below summarizes the descriptive statistics of the study variables. The purpose of this descriptive analysis is to identify the descriptive characteristics of the explanatory and control variables in our study model. These characteristics concern the average, standard deviation, minimum, and maximum. The descriptive statistics of the different variables for the panel Euro zone countries and for MENA countries are presented in Table 1.On average, the highest levels of unemployment (13.8), public dept. (86.18); budget deficit (3.04), as well as is the case for MENA countries. On standard deviation, euro zone countries is the more volatility compared with the MENA countries the highest levels of unemployment (5.26), public debt (40.52); budget deficit (6.45).

| Eurozone countries | Mena countries | |||||||

|---|---|---|---|---|---|---|---|---|

| Mean | SD | Min | Max | Mean | SD | Min | Max | |

| UNEM | 11.88 | 5.26 | 3.66 | 17.47 | 13.78 | 4.78 | 8.1 | 29.5 |

| CTS | 9.57 | 7.45 | 2.1 | 7.22 | 4.37 | 15.95 | -6.924 | 9.62 |

| D | 86.18 | 40.52 | 25.5 | 183 | 68.7 | 31.72 | 2.85 | 219.8 |

| BD | 2.85 | 6.45 | -1.2 | 7.2 | -3.04 | 5.84 | -3.46 | -8.96 |

| OP | 82.77 | 44.39 | 35.51 | 216.7 | 75.84 | 28.25 | 32.98 | 149 |

| GDP | 6.88 | 5.39 | -9.58 | 32.43 | 6.43 | 12.24 | 2.04 | 12.41 |

| INF | 5.39 | 2.84 | 1.7 | 5.41 | 5.9 | 5.97 | -1.69 | 8.67 |

| GFCF | 21.95 | 4.02 | 11.44 | 31.05 | 22.13 | 4.01 | 11.44 | 31.05 |

| MMR | 5.79 | 4.63 | -4.26 | 18 | 3.34 | 1.72 | 0.27 | 8.029 |

Table 1: Summary statistics.

Panels unit root test

The decision rule is that the H0 assumption (all series are non-stationary) is rejected if p-values are inferior to 5%. The results of the hadri stationarity test show that almost all the variables are stationary in level (I(0)), i.e. (UNEM P,BD,D,GDP,INF,OP,FBCF,MMR) while only the variable CTS is not stationary.

The Table 2 above shows the result of unit root test of HADRI applied in the five MENA countries data (Tunisia, Algeria, Morocco, Egypt, Jordan) and six euro zone countries (Spain-France-Portugal-Cyprus-Ireland-Greece).

| MENA countries | Euro zoneuro countries | |||

|---|---|---|---|---|

| Variable | T-Statistics level | p-value | T-Statistics level | p-value |

| UNEMP | 25.2759 | 0 | 12.7068 | 0 |

| CTS | 5.168 | 0 | -0.4575 | 0.6763 |

| D | 24.129 | 0 | 20.857 | 0 |

| BD | 5.1157 | 0 | 1.8067 | 0.0354 |

| OP | 17.306 | 0 | 27.591 | 0 |

| GDP | 1.7611 | 0.03 | 3.0915 | 0.001 |

| INF | 14.382 | 0 | 2.6805 | 0.0037 |

| FBCF | 14 | 0 | 15 | 0 |

| MMR | 23.638 | 0 | 27.535 | 0 |

Table 2: Results of panel unit root tests.

Poolability test

The calculated file statistics presented in the table show that it is superior to the statistics read from the Fischer table, at the 1% threshold; we can therefore reject the null hypothesis of a perfectly homogeneous structure and accept h1 the hypothesis of the presence of an individual effect in the panel data. Scalar fisher= ((scrh0-scr)/ (dlh0-dlh1))/ (scr/dlh1).

Table 3 and Table 4 shows that the Fisher statistics calculated for the Eurozone countries and MENA countries are higher than the statistics reading from the Fischer table, at a 5% threshold; we can therefore reject the null hypothesis of a perfectly homogeneous structure and accept h1 the hypothesis of a perfectly heterogeneous structure.

| Scrh0 | Scrh1 | dlh0 | dlh1 | dh0-dh1 | (Scrh0-Scrh1)/ (dlh0-dh1) | Scrh1/dh1 | Fisher calculated for each country | |

|---|---|---|---|---|---|---|---|---|

| Tunisia | 2816.07 | 32.08 | 126 | 18 | 108 | 25.78 | 1.78 | 14.46 |

| Algeria | 2816.07 | 164.53 | 126 | 36 | 90 | 29.46 | 4.57 | 6.45 |

| Morocco | 2816.07 | 175.34 | 126 | 54 | 72 | 36.68 | 3.25 | 11.3 |

| Egypt | 2816.07 | 188.69 | 126 | 72 | 54 | 48.66 | 2.62 | 18.57 |

| Jordan | 2816.07 | 237.26 | 126 | 90 | 36 | 71.63 | 2.64 | 27.17 |

ficher's test 27.17

Fisher's test for fixed effect 22.47

f tabuler=(5.90)=2.71

Table 3: Poolability test MENA countries.

| scrh0 | Scrh1 | dlh0 | dlh1 | dh0-dh1 | (scrh0-scrh1)/ (dlh0-dh1) | Scrh1/dh1 | Fisher calculated for each country | F(6.180)=2.59 | |

|---|---|---|---|---|---|---|---|---|---|

| France | 2816.07 | 106.29 | 153 | 18 | 135 | 20.07 | 5.9 | 3.4 | Fs>FC |

| Spain | 2816.07 | 275.43 | 153 | 36 | 117 | 21.71 | 7.65 | 2.84 | Fs>FC |

| Portugal | 2816.07 | 333.02 | 153 | 54 | 99 | 25.08 | 6.17 | 4.07 | Fs>FC |

| Ireland | 2816.07 | 407.68 | 153 | 72 | 81 | 29.73 | 5.66 | 5.25 | Fs>FC |

| cyprus | 2816.07 | 446.13 | 153 | 90 | 63 | 37.62 | 4.96 | 7.59 | Fs>FC |

| Greece | 2816.07 | 575.52 | 153 | 108 | 45 | 49.79 | 5.33 | 9.34 | Fs>FC |

Fisher Test 9.34

Fisher Test fixed effect 20.07

Table 4: Poolability test eurozone countries.

Breusch and pagan

Test The Breusch-Pagan statistic is obtained after estimation of the random effects model. It is used to test the significance of the random effects model. If the probability of the BreuschPagan statistic is less than the specified threshold, the random effects will be significant overall. The test is based on the following assumptions:

H0: Absence of random effects

H1: Presence of random effects

The breush pagan test result calculated for the two groups of countries (Euro zone and MENA countries) to show a probability greater than 5%, therefore, the presence of individual random effects is confirmed. This test carried out on the random effects model gives the following result The brush pagan test obtained after regression under random effect individual and period presents a probability > 5%, therefore rejects h0 and accepts h1. We can say that the data deviate significantly from homoscedasticity (Table 5).

| Test de Breusch-pagan | MENA countries | Eurozone countries |

|---|---|---|

| Random effect individual | Var(u)=0 chibar2(01)=0.00 Prob>chibar2=1.0000 | Var(u)=0 chibar2(01)=0.00 Prob>chibar2=1.0000 |

| Random period effect | chibar2(01)=0 Prob>chibar2=1 | chibar2(01)=0 Prob>chibar2=1 |

Table 5: Summary of breusch-pagan specification results test.

Hausman test

The displayed test probability is less than 5% (0.000) for both groups of countries (MENA and Eurozone ), so the fixed-effect model is preferable to the random-effect model.

Table 6 present the estimated results a model based on fixed effect for MENA countries and Euro zone countries. The endogenous variable is the unemployment rate and we have used seven control variables: public debt (D) - budget deficit (BD) - current GDP growth rate - gross fixed capital formation (GFCF ), money market rate (MMR), openness rate (OP). For the euro zone countries, the critical threshold of a sustainable primary balance (CTS) has a positive and no significant impact on the unemployment rate.

| MENA countries | Eurozone countries | |

|---|---|---|

| variable | Fixed effects | Fixed effects |

| CTS | -0.01 (0.693)* | 0(0.948)* |

| D | 0.07(0000)*** | 0.020.034** |

| BD | 0.17(0.001)*** | 0.130.078* |

| OP | -0.06(0.009)*** | -0.050.038** |

| GDP | 0.03(0.379)* | 0.1920.262* |

| INF | 0.05(0.369)* | -0.280.005*** |

| CFCF | -0.02(0.167)* | -0.680*** |

| MMR | 0.26(0.167)* | 00.998* |

| _cons | 13.5 | 29.7 |

| prob>f=0.000 |

Table 6: Fixed effect result (Unemployment as dependent variable).

The impact of public debt (D) on the unemployment rate is significantly positive at a 5% threshold. The budget deficit (BD) has a positive and statistically significant impact at a 10% threshold. Therefore, we note that the openness rate (op) and gross fixed capital formation (GFCF ) have a significantly negative effect with the unemployment rate. The money market rate (MMR) has a positive, but statically insignificant impact. However, for the MENA countries, we note that the (CTS) has a negative and significant effect at a 1% threshold on the unemployment rate. Public debt has a positive and significant impact at a 1% threshold with the unemployment rate. The budget deficit shows a positive and significant impact with the unemployment rate. The opening rate coefficient shows a negative and significant impact with the unemployment rate. Therefore, we note that the variables GDP, MMR, GFCF have a positive but statistically no significant effect.

Economic phenomena of some complexities are labeled by a set of variables, but their modeling usually requires more than one relationship, or equation, linking these quantities, is therefore referred to as simultaneous equation models. A distinction is then made between endogenous variables, which are determined by the model, and exogenous variables determined or fixed outside the model. Modeling operates in three phases: the design, i.e. the writing or model specification that estimates the model equations, using appropriate techniques for the resolution of the model, prior to its use for simulating or forecasting of course .In reality things are not sequential and development of a model is a back and forth process.

Identification conditions

The method of estimation in simultaneous equation models depends on the model identification criterion, (Bourbonnais, 2002). Thus, the following three cases can be distinguished:

If the model is under-identification, no estimation is possible. The model must then be specified.

If the model is identified, correctly indirect least squares or double least squares can be applied.

If the pattern is over-identified, double least squares are applied.

Result of simultaneous equation panel data models

In this section we will check the link between the budget deficit, unemployment and public debt for the MENA countries and euro zone countries, so the question that now assumes that it is the impact of the sustainability of public debt on unemployment? Is there really a relationship between these three variables? How can we conclude this relationship?

The Table 7 above correspond the results of our model estimation from the simultaneous equation mechanism. We have to recall that all estimates were made using STATA software. We can recall that the purpose of this study is to test the relationship between the budget deficit, the public debt and the unemployment rate.

| Eurozone countries | MENA countries | ||||

|---|---|---|---|---|---|

| Variable | Coefficient | (p-value) | Coefficient | (p-value) | |

| EQ1 | L_UEMP | 0.8540109 | 0*** | 1.09109 | 0*** |

| D | 0.0208236 | 0.019*** | 0.01369 | 0.001*** | |

| BD | -0.0766985 | 0.04*** | -0.2007 | 0.001*** | |

| b100 | 1.727895 | 0.011*** | -2.2195 | 0.011*** | |

| EQ2 | Ldb | 0.7921889 | 0*** | 0.3712 | 0.001*** |

| UEMP | -0.1196344 | 0.064* | 0.44017 | 0.001*** | |

| D | 0.019485 | 0.009*** | -0.6148 | 0*** | |

| GDP | 0.5164925 | 0.001*** | 0.09638 | 0.008*** | |

| INF | -0.1245475 | 0.187* | -0.1936 | 0.002*** | |

| MMR | -0.0346205 | 0.671* | 0.16724 | 0.282* | |

| b200 | 1.215648 | 0.269* | -7.8768 | 0*** | |

| EQ3 | Ldp | 0.9636146 | 0*** | 0.86528 | 0*** |

| UEMP | -0.2085792 | 0*** | 0.13884 | 0.722* | |

| CTS | -0.4199577 | 0*** | -0.1864 | 0*** | |

| BD | -0.0332818 | 0.9* | -0.7493 | 0.115* | |

| OP | 0.0017862 | 0.945* | 0.01563 | 0.52* | |

| GFCF | -0.6839485 | 0.004*** | -0.0029 | 0.989* | |

| b300 | 26.91082 | 0.001*** | 3.29691 | 0.741* | |

| Hansen's J chi2(12)=14.0604 (p=0.2969) | Hansen's J chi2(12)=9.3011 (p=0.6770) | ||||

Note: *** Significant at 1 percent; ** Significant at 5 percent; *Significant at 10 percent

Table 7: Results estimation by simultaneous equations.

We then have to analyses the effects of an indicator on the other two variables and the same work will be done with the other variables to be explained. Indeed, with regard to the first equation (Eq1) the results show that: For both groups of countries, the public debt ratio (D) acts positively with the unemployment rate at a 1% threshold, implying that a very high public debt ratio can hamper economic growth and consequently affect investment negatively and employment creation, especially in unstable economic context characterized by a drop in demand [21-25].

Similarly, the budget deficit coefficient has a negative and statistically significant effect on the unemployment rate. Here it implies the effectiveness of fiscal policy in terms of boosting demand and reducing unemployment rates. At the level of the second equation (Eq2), we notice that the unemployment coefficient has a positive and statistically significant effect with the budget deficit at a 10% threshold for the MENA countries; on the other side, it acts negatively and statistically significant at a 5% threshold from Euro zone countries. With the weakness of economic activity, public administrations are capturing savings at the expense of the financing of private companies (the so-called "crowding out effect"), which will have a negative impact on employment rate. Government debt in the euro area has a positive impact on the budget deficit because its coefficient is statistically significant. This shows that any increase in the government debt ratio causes the budget deficit to increase. Not least, we have found that the public debt ratio in the MENA countries is negative and statistically significant at a 1% threshold with a budget deficit, which shows that today a high debt can provide resources to finance productive public spending (such as infrastructure investments) that can raise the path of growth [26].

The results of the third equation show that the influence of unemployment rates on government debt in the euro zone is negative and statistically significant at a 1% threshold. This explains why the increase in unemployment expenditure after an economic crisis helps to sustain demand for goods and services and thus to mitigate the effects of the crisis on the turnover of companies. In fact, unemployment benefits in the euro zone countries present an economic mechanism with a regulator, passive and counter-cyclical activity. When the economy is expanding, taxes rise as consumption and employment rise and social benefits decrease as unemployment decreases. On the other hand, we notice that the unemployment rate in the MENA region has no effects on the public debt [27].

In this research based, we have tried to contribute to the resolution of a fundamental question: is there a link between unemployment, public debt and budget deficit for the six selected countries of the euro zone countries as well as for the five privileged countries of the MENA region? Therefore, we should note that no empirical study has been done so far to determine the interactions between these three variables and in order to analyze the interdependence between these systems of equations, we have found that only the simultaneous equation model is able to allow us to analyze the dynamics between its different variables. The variables used in our econometric model are: the critical threshold of the sustainable primary balance, the budget deficit, the public debt, unemployment, inflation, the current GDP growth rate, the money market rate, the fixed capital formation, the openness rate. The study lasted from 1990 to 2016. Indeed, the results of the model estimation for the six euro zone countries (France, Spain, Portugal, Greece, Cyprus and Ireland) confirm that there is a two-way relationship between unemployment and debt. Similarly, there is a two-way relationship between the budget deficit and unemployment. At another level, we note a unidirectional relationship from budget deficit to public debt. However, for the five countries of the MENA countries, we have found a unidirectional relation going from public debt to unemployment, a twin directional relation between deficit and unemployment and a unidirectional relation going from debt to the deficit. According to the results obtained we can assert that Keynesian and neo-classical macroeconomic policies have shown limited in the fight against unemployment for both groups of countries: these policies have not made it possible to eradicate unemployment. Therefore, it is important to develop a macroeconomic policy that promotes growth, combined with appropriate structural policies aiming at changing the rules of the game in factor markets, as well as to placing greater emphasis on active labor market policies and make them effective.

Very few studies sought to tackle the topic of this study, or at least this topic was not dealt with from all angles. This paper is an addition to existing literature as it contributes to recognize the dynamic links between three macroeconomic variables: public debt, unemployment and budget deficit. Moreover, this study is among very few studies that use regression analysis in the period between (1990) and (2016) to highlight the aforementioned relationship.

Business and Economics Journal received 6451 citations as per Google Scholar report